MOOC: Introduction to environmental auditing in the public sector

2.1. The audit cycle and an environmental audit as a performance audit

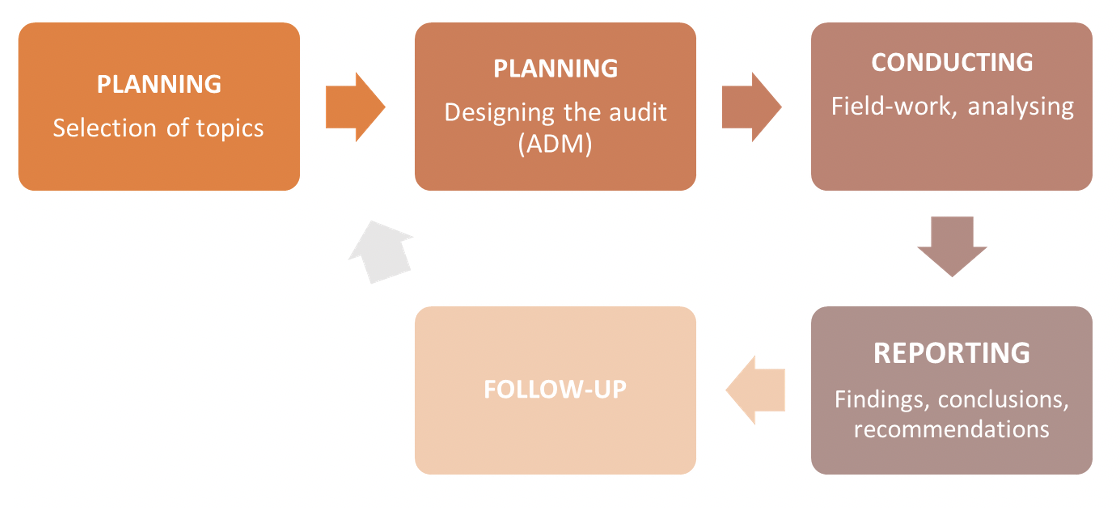

The audit cycle

For the auditor, conducting an audit is quite a clear and defined process with its beginning and end (issuing an audit report). The main phases of the audit according to the ISSAI 300 are:

a) planning, including selection of the topic and designing the audit

b) conducting an audit

c) reporting

d) follow up

In principle, the audit process can be described as a cycle, like many policy processes, where continuous improvement is a natural evolution. An environmental audit cycle does not differ from any other performance audit cycle.

Although an audit process is usually described as a cycle, it is often not a continuous cycle. In the follow-up phase, auditors may decide to repeat an audit with the same focus if the situation has not improved. More often, the subsequent audit in the same area will have a different focus because the situation has changed.

In this Module no. 2 and in the following Modules no. 3 and 4, we will follow this cycle of the audit process:

Figure. Audit process (source: ISSAI 300)

Environmental audit as a performance audit

Although environmental audits can be conducted as financial or compliance audits, they are most commonly conducted as performance audits. Therefore, the principal questions in environmental audits are generally the same as those in performance audits:

- Have the right things been done?

- If so, have they been done in the right way?

- If not, what are the causes?

Environmental audits also often follow the concept of the 3 Es – economy, efficiency and effectiveness – which form the basis of a performance audit. The 3 Es are explained in the figure below.

Figure. The concept of the 3 Es: economy, efficiency and effectiveness

The 3 Es bring another dimension into an environmental audit – money. Environmental programmes can be among the biggest programmes in a country, often involving international investments or aid, e.g. investments in the energy sector, transport or water infrastructure.

|

Tip for an auditorAuditors may ask: Was the money used for the purpose it was provided for? Was the money allocated to the programme in a way that ensures the delivery of outcomes? |

It is not unusual for money to vanish from programmes and for no success to be met in achieving targets.

|

Reading suggestion!‘Addressing Fraud and Corruption Issues when Auditing Environmental and Natural Resource Management: Guidance for Supreme Audit Institutions’ (INTOSAI WGEA, 2013) |

| Thinking exercise – impact of the auditDecisions made during all audit stages affect the final impact of the audit. Ways of increasing the impact of an audit are well described in the article ‘How to increase the impact of environmental performance audits’ (J. Reed, J. Cinq-Mars, International Journal of Government Auditing, April 2014, pp. 17-23). Read the short article (first three pages). What are the foundations of a successful performance audit? What are the tips for the planning phase? Could you use some of the suggestions to improve your own audit work? |

|

Reading suggestion!To read more about performance audits you may have a look at the following: INTOSAI (2019) ISSAI 300 Performance Audit Principles INTOSAI (2019) GUIDE 3920. The Performance Auditing Process INTOSAI IDI (2021): Performance Audit: ISSAI Implementation Handbook NB. The handbook is also available in Spanish, French and Arabic. |

The main source of guidance for an environmental audit is the International Organisation of Supreme Audit Institutions Working Group on Environmental Auditing (INTOSAI WGEA).

Four guidance documents in the field of environmental auditing have been adopted by INTOSAI as part of the Framework of Professional Pronouncements.

Joint and cooperative audits

Environmental problems are often cross-border and regional and require joint action. Therefore, there are many examples of joint, parallel and cooperative audits on environmental issues, where two or more SAIs are involved in auditing a common environmental problem.

Examples of joint and cooperative audits:

- OLACEF – Coordinated Audit on Sustainable Development Goals (Auditoría Coordinada sobre Objetivos de Desarrollo Sostenible, 2018) and others

- PASAI – Pacific regional report on the cooperative performance audit into solid waste management (2010) and others.

- AFROSAI – Joint environmental audit on saving lake Chad, 2015 (video: 6:39)

- EUROSAI – Joint report on air quality, 2019.

|

Reading suggestion!INTOSAI guide 5203 Cooperation on audits of international environmental accords |